From a hard-hitting interview with Jack Mallers on Savvy Finance, the investment rules many of us grew up with are cracking. This article breaks down the case Mallers lays out: the traditional 60/40 mix of stocks and bonds is failing institutional savers, and crytocurency, bitcoin is emerging not as a speculative punt but as a strategic reserve asset. Read on for the data, the policy moves, and what this means for long-term portfolios.

Table of Contents

- Key takeaways

- Why the 60/40 myth is breaking

- Policy levers: How governments are responding

- Institutional adoption: Harvard, Meta Planet and the new reserve buyers

- The portfolio question: How much crypto exposure is sensible?

- Data points that back the shift

- What to watch next (practical checklist)

- Conclusion: A new monetary era or a passing vogue?

Key takeaways

- The classic 60% stocks / 40% bonds portfolio is under severe strain: multi-year bond losses and a commercial real estate collapse have eroded long-duration savings.

- Policy changes — notably broader access to Bitcoin and gold in retirement plans — are being framed as a rescue strategy for battered savings accounts.

- When top institutions and endowments allocate to crytocurency, bitcoin it signals a structural shift from fiat-denominated assets to scarce digital money.

- For anyone responsible for multi-decade liabilities (pensions, endowments, sovereign funds), diversifying into non-fiat, non-bond assets is becoming an operational necessity — not an ideological choice.

Why the 60/40 myth is breaking

For decades, the 60/40 model worked because bonds reliably provided stability while equities provided growth. That equilibrium depended on low debt, stable inflation expectations, and positive real bond returns. Those assumptions are no longer holding.

Key points Mallers highlights:

- Five straight years of losses in many bond buckets have turned the “stable” half of the portfolio into dead weight.

- Commercial real estate valuations have been written down as much as ~85%, inflicting direct losses on municipal and corporate pensions.

- Much of the broad market's apparent nominal gains are a function of dollar debasement; measured in real terms (relative to a stable monetary standard) most of the S&P 500 constituents have not kept pace with inflation.

Real-world consequences

When pensions and endowments are underwater, public services get starved. Mallers points to underfunded police forces, broken municipal budgets, and strained public sector services as downstream effects. In short: broken money systems create social costs.

Policy levers: How governments are responding

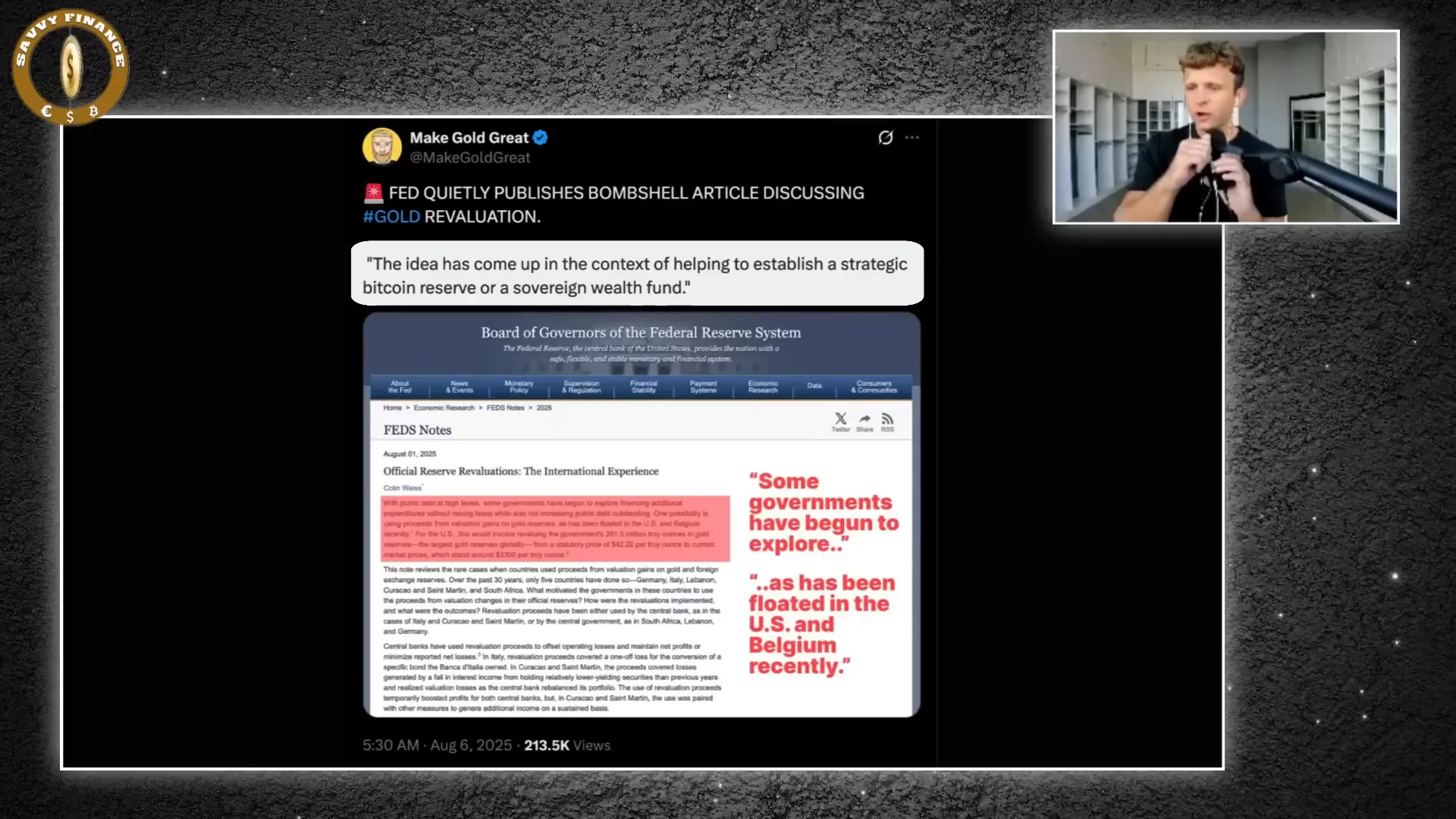

Rather than allowing portfolios to slowly wither, policymakers are taking active steps. Two critical moves highlighted:

- Executive actions expanding retirement plan options to include Bitcoin and gold. This opens a channel for savers to gain exposure to scarce assets inside their 401(k) accounts.

- Central bank / treasury discussions about balance sheet transformations — including reassessing gold valuations — as a way to create fiscal space and potentially seed strategic reserves that could include Bitcoin.

These moves change the universe of possible portfolio responses. If the only way to arrest erosion is to dilute the currency (debase the dollar) while giving savers realistic exposure to appreciating stores of value, then allowing crypto and gold into tax-advantaged accounts becomes a policy tool — a liquidity escape valve, as Mallers puts it.

Institutional adoption: Harvard, Meta Planet and the new reserve buyers

Institutional interest matters because these are conservative, long-duration allocators. When universities, sovereign funds, and corporations put nine-figure positions on their balance sheets, it changes the narrative from “speculation” to “capital preservation.”

Notable examples:

- Harvard disclosed a six- or seven-figure (reported as over $100M) position — the kind of vote of confidence that changes institutional peer behavior.

- Meta Planet and other corporations steadily accumulating large Bitcoin treasuries demonstrate that corporate treasury strategy is shifting toward assets that cannot be inflated away.

Why this matters for pensions and endowments

Pensions and endowments are fiduciaries with long horizons. If long-duration bonds and many equities no longer protect purchasing power, rotating even a fraction of reserves into scarce assets can dramatically alter long-term outcomes. Mallers argues that this shift isn't marginal — it's foundational.

The portfolio question: How much crypto exposure is sensible?

Mallers challenges the popular “1% allocation” take. His argument is blunt: if you truly believe Bitcoin is superior money, allocating a token percentage while keeping the vast majority in assets that structurally lose real value doesn't align with long-term preservation goals.

That said, practical implementation should consider:

- Fiduciary duty and regulatory guidance

- Liquidity needs and volatility tolerance

- Custody and security arrangements for digital assets

- Gradual, audited allocations as part of an overall risk-managed framework

Data points that back the shift

- Five consecutive years of losses in many bond classes.

- Commercial real estate markdowns up to ~85% in some pockets.

- Most of the S&P 500 (493 companies excluding mega-cap winners) expected to deliver 2–3% net income growth — often below real inflation.

- Over 200 public companies now holding Bitcoin on their balance sheets; recent multi-million-dollar corporate buys continue to accumulate supply.

What to watch next (practical checklist)

- Regulatory guidance on holding digital assets in retirement accounts and fiduciary best practices.

- Further institutional disclosures from endowments, sovereigns, and corporate treasuries.

- Market reaction to any formal moves by central banks or treasuries to revalue gold or create sovereign digital reserves.

- Product availability that lets ordinary savers access crytocurency, bitcoin inside tax-advantaged wrappers with professional custody.

Conclusion: A new monetary era or a passing vogue?

The case Mallers lays out is not a price call — it's structural. Broken bond markets, a stretched equity universe, collapsing real estate valuations, and active policy responses are combining to create a powerful incentive for institutional diversification into scarce, non-sovereign assets.

Whether you call it crytocurency, bitcoin or digital money, the practical implication is clear: institutions that must preserve value for decades are starting to treat Bitcoin like insurance against currency debasement. That changes capital flows and, over time, the architecture of global savings.

"The sixty forty portfolio is dead." — a blunt, repeated refrain that captures the gravity of the shift.

Do you agree that the 60/40 portfolio is collapsing and that crytocurency, bitcoin deserves a strategic allocation for long-term savers? I encourage you to watch the full interview on the Savvy Finance channel and weigh the data for yourself — then consider how your own long-term plans might adapt.

Why the 60/40 Portfolio Is Dead: How crytocurency, bitcoin Is Reshaping Retirement Strategy. There are any Why the 60/40 Portfolio Is Dead: How crytocurency, bitcoin Is Reshaping Retirement Strategy in here.